Study: Remittance Flows from the Czech Republic and their Development Impact

A) Why remittances?

The development potential of remittances and the role of non-governmental organisations – An introduction

Tereza Rejšková

Multicultural Center Prague

This study aims to present the issue of remittances – transfers of money earned by migrant workers abroad back to their countries of origin – in the context of the development agenda. Focusing on the situation in the Czech Republic, the study presents the results of research that has been carried out among migrants and non-governmental organisations.

But how does the problem of remittances interact with the field of development co-operation, and how does this study relate to other studies analysing the effectiveness of non-governmental organisations? Part of the answers can be found in a text by Robert Stojanov who supports a general view of remittances as an effective tool of economic development in less developed countries. Even a brief glance at the figures justifies this argument. The World Bank estimated that global remittances to developing countries reached $305 billion in 2008.[1] This astonishing figure exceeds the volume of funds earmarked for these countries in the form of development aid[2] or foreign direct investment. The GDP of some of these countries is dependent on remittances. It cannot be said that remittances always and only increase the standard of living in countries of origin (part of the funds cover debts related to migration; remittances also bring certain disadvantages in macroeconomic terms). Still, remittances are indisputably an important aspect of development.

Put shortly, the development potential of remittances can be enhanced both in destination countries and in countries of origin. In destination countries, the goal should be to minimise migrant income deductions and losses (above all by lowering the fees for international transactions, or by reducing wage deductions going to employment agencies). As for the countries of origin, the families of migrants should be able to use financial services enabling them to invest money or deposit it in a bank account under favourable conditions. In reality, these families often incur losses because such financial services are unavailable. As the World Bank’s Donald F. Terry pointed out at a recent seminar on remittances - “It is expensive to be poor”.

Why should the Czech Republic be concerned with remittances at all? The Czech Republic has become an immigration country, with a large number of migrants coming here to work. At the moment, there are about 440,000 foreigners with long-term or permanent residency status. Many of them earn a living here and send part of the money that they earn back to their families and friends in the form of remittances. The issue of remittances is complex, as it touches on both development and migration policies, and its potential has increasingly caught the interest of various players, including the Czech Ministry of Finance, the Czech Statistical Office, the Czech National Bank, commercial banks, academic institutions and non-governmental organisations that work (often face-to-face) with migrants. We tried to encourage a relevant and broad discussion of the issue within the FoRS project which included, among other events, the seminar “Remittance Flows from the Czech Republic and their Development Impact”[3]. Despite positive feedback, it remains unclear how much participating institutions will co-operate in the future. Still, the seminar enabled a joint discussion between various institutions, which have previously communicated with each other to a very limited extent even though they are public institutions. As a result, these institutions have identified their joint interest in particular problem areas and have started to co-operate. Some unusual forms of co-operation were established, such as between the Czech Statistical Office and experts from the non-governmental sector. The fact that the seminar was organized by non-governmental organisations which operate outside complex bureaucratic structures, which often limit any access to essential information, seems to be an advantage. For example, the Interior Ministry has learnt from the website of a non-governmental organisation that the Finance Ministry has also been dealing with the issue of remittances. By contrast, non-governmental organisations often strive to make all information as accessible as possible, as quickly as possible.

We would be particularly satisfied if we could establish the idea of migrants participating in the decision-making of Czech institutions. We believe that non-governmental organizations, which often take up the role of defending migrants’ rights and mediating between migrants and state representatives, have a greater chance of gaining migrants’ trust and persuading them to participate in the monitoring of remittances, or in potential information campaigns and other programmes. Nevertheless, we are aware that this may also be difficult because migrants are often reluctant to talk about financial issues.[4] Therefore, informing migrant associations and individual migrant representatives about the benefits that active co-operation, e.g. with public authorities, has for migrant communities could be a key task for non-governmental organisations. At the same time, it is important to put pressure on public authorities to listen to migrants. Migrants have been completely excluded from the decision-making process at the level of state institutions thus far. This could have a negative impact - measures may be taken that no one will be interested in.

In this sense, non-governmental organisations are able to voice migrants’ views when trying to influence political decisions. Many Czech non-governmental organisations already have very good experience in this regard. For the time being, it is uncommon for migrant communities and civic organizations in the Czech environment to engage in policy-making. Czech non-governmental organisations could share their experience with these associations.

Non-governmental organisations often offer migrants individual counselling (legal, social, psychological) and thus have the opportunity to learn about the reality of their life from individual perspectives. For understandable reasons, public authorities and other representatives do not encounter these micro-perspectives. Hence, in this sense, co-operation between public and non-governmental sectors could be very useful. Nevertheless, it is important for non-governmental organisations to strengthen public sector trust in them and a willingness to establish partner relations.

One of our sub-tasks was to evaluate the activities of non-governmental organisations so far and assess their potential to operate effectively in the field of remittances. We have contacted almost all the Czech organisations that work with migrants, trying to find out more about their experience with counselling on money transfers and related problems. However, most organisations do not deal with these kinds of problems, mainly due to a lack of interest from migrants. Above all we have considered the extent to which non-governmental organisations could serve as a source of information for optimal means of money transfer, and hence help to increase the development impact. Some organisations have stated their willingness to take part in a potential information campaign. Still, it remains to be seen whether institutions, which migrants themselves do not consult when trying to find out more about remittances, would be suitable distributors of such information. Non-governmental organisations stated that clients seek their assistance mostly when they find themselves in an emergency situation in the Czech Republic and need to arrange a money transfer from their relatives in their countries of origin. This supports the hypothesis that migrants in the Czech Republic mainly turn to non-governmental organisations in moments of crisis, which limits the scope of their action to a great extent. It would be desirable to change this set-up in the future. In addition, migrants consider the topic of personal finances very sensitive and do not want to discuss it among themselves, let alone among strangers.

To be comprehensive, it is important to note that we have not focused on projects that could be implemented in countries of origin (such as the promotion of financial literacy in the families of migrants, or connecting families with micro-financial institutions).

Despite the shortcomings that non-governmental organisations face in this field, it is indisputable that these organisations could play a significant role in increasing the development potential of remittances sent from the Czech Republic. This is because their primary objective is to help migrants without bias or agenda (as could be the case with public or academic institutions).

Structure of the study

The study comprises this introduction followed by three main parts. In the first part, Robert Stojanov introduces the issue from a global perspective, presents basic data and relevant research about remittances and outlines their position in the development paradigm.

In the second part, Pavlina Šolcová maps the research and political efforts concerning remittances in the Czech Republic up to the present. There is a general lack of relevant data, as analyses and discussions of the issue of remittances at an international level have only recently appeared. No wonder therefore that there has been almost no research into this topic in the Czech Republic so far.

In order to increase the development potential of remittances, it is absolutely crucial to find out more about the situation: the numbers of migrants sending money home; the way they channel the funds, the problems migrants and their families encounter in countries of origin, etc. Our aim was to map innovative research on remittances sent from the Czech Republic; to use our own well-established contacts within the migrant community and contribute with an authentic research project based on detailed individual interviews. The project results can be found in the third, pivotal part of this study. In this part, Blanka Tollarová and Tereza Rejšková present their research pilot, conducted between December 2008 and February 2009, which uncovered the experiences of migrants, migrant associations and non-governmental organisations in relation to the sending of remittances. The results reveal the problems associated with sending remittances and uncover some facts that are specific to the Czech environment.

It is important to bear in mind that efforts to increase the development potential of remittances and their regulation in the Czech Republic are only just beginning. Our primary objective is to learn more about the situation and avoid preventable mistakes in the future, rather than to assess the projects and measures hitherto undertaken. Our second goal is to provide information to any parties that may be interested in conducting further research or who might wish to coordinate their actions with a view to avoiding the waste of energy and financial resources caused by imperfect communication among different intitutions. We believe that this study will make a valuable contribution to the discourse on the approach that institutions in developed countries, including CSOs, should take with regard to remittances and developing countries.

B) The development potential of remittances – a brief outline of the issue[5]

Robert Stojanov

Faculty of Regional Development and International Studies, Mendel University in Brno

B1. Introduction

The relation between international migration and development is currently discussed by development and migration studies specialists. The idea of reducing socio-economic differences through the development of economically less developed countries and through liberalization of workforce mobility has been present in the political agenda for the last ten years. Remittances figure highly in discussions on this topic.

Based on an analysis of selected secondary sources, the author of this text comes to the conclusion that international migration flows in the form of remittances have a predominantly positive impact on the development of economically poor regions. The first part of this article outlines some of the current international migration trends. The second part provides a brief analysis of the conclusions that studies on the impact of remittances on development and poverty in economically poor countries have drawn.

B2. International migration as a global phenomenon

The migration of populations is a process that significantly influences the long-term development of mankind. According to the estimates of United Nations the number of international migrants[6] was 191 million in 2005, which represents about 3 percent of the world’s population. The total number of international migrants rose by 15 million in 2005, compared with estimates for the year 2000 (UNPD 2005)[7]. The traditional routes and intensity of migration flows vary according to the level of development in individual countries. The development paradigm – which contains the idea of progress in the sense that “the situation develops for the better” - thus gains a firm position in considerations of migration. In this way Skeldon (1997)[8] points to the fact that basic development indicators, such as life expectancy, or access to health services and education, improved for a large part of the world’s population over the last 60 years. However, this is not applicable to all countries and regions. The reality of “insufficient” or minimum development encourages further research.

The present era of global migration began at the end of World War II. Its current manifestations are closely related to new means of communication and transportation, which, better and faster than ever before, reduce the role of distance between countries of origin and countries of destination. The falling costs of international telephone calls and of international transport, as well as the introduction of fax and e-mail communication, have enabled migrants to stay in touch with their country of origin in far more intensive way. This lowers the pressure on migrants to relocate their entire family to a new destination. International migrants are thus able to gain the best from both worlds – they earn high income in areas with high prices and spend it in countries with low incomes and prices. In addition, they have a greater chance of preserving their cultural values and family ties (Hugo 2003)[9].

The highest intensity of migration flows is seen within the regions of developing countries. But from the point of view of the international migration-development nexus, it is important to analyse migration flows between economically advanced and developing regions. According to Massey et al. (1993)[10], these flows started to soar at the end of the 1960s, as immigrants from Asia, the Caribbean and the Middle East were heading for Western Europe.

The total estimated number of international migrants has more than doubled, from 75.5 million in 1960 to 190.6 million in 2005. The relative increase in migrant numbers for the same period, calculated as a ratio of the total population of the Earth, is a lot more modest, rising from 2.5 percent in 1960 to 3.0 percent in 2005. The ratio has not changed very much in the last two decades (see Table B.1).

Table B.1 Estimated number of international migrants worldwide and their percentage share of the world population (1960 - 2005)[11]

|

Year |

Estimated international migrant numbers |

Share of international migrants in world population (%) |

|

1960 |

75.463,352 |

2.5 |

|

1965 |

78.443,933 |

2.4 |

|

1970 |

81.335,779 |

2.2 |

|

1975 |

86.789,304 |

2.1 |

|

1980 |

99.275,898 |

2.2 |

|

1985 |

111.013,230 |

2.3 |

|

1990 |

154.945,333 |

2.9 |

|

1995 |

165.080,235 |

2.9 |

|

2000 |

176.735,772 |

2.9 |

|

2005 |

190.633,564 |

3.0 |

Source: UNPD data (2005)

Most international migrants stay in Europe (more than 61.1 million), followed by Asia (53.3 million), North America (44.5 million) and Africa (17.1 million). In 2005 an enormous increase in migration was registered in Europe, where the relative migrant figures doubled, from 18.9 percent in 1960 to 33.6 percent. For this period, the absolute figures increased by almost four times (UNPD 2005).

Globalisation has played a significant role in changes to the form of international migration that have been noted in recent decades. Supposedly, the most important change is that pull factors have become as relevant as push factors. Migration flows are driven not only by the combination of poverty, demographic pressures and other push factors, but also by pull factors – the Western comfort displayed in movies and TV programmes, the entertainment and consumer goods sold on local markets. Hence, migrants may wish to increase the quality of their life not only in economic but also in social and cultural terms (IOM 2003)[12].

A fairly new phenomenon is the growing number of women in international migration flows. Women currently account for almost a half of international migrants and dominate migration flows to economically advanced countries. Simultaneously, women are among the most vulnerable migrant groups, above all in the area of human rights violation. Women increasingly migrate alone, and in practice they are often the main earners for the family left behind. This trend is expected to continue because the demand for labour in traditional female occupations in industrialised countries has been growing. These occupations encompass jobs in household, nursing and caring services, cleaning, entertainment and the sex industry, retail jobs and work in factories. The migration of women also affects countries of origin, as it tends to increase the number of divorces and widowed persons, cause childlessness or solitude. By contrast, migration brings many women better access to education, makes them aware of their rights and improves their chances of finding a job and gaining new experiences (GCIM 2005)[13].

There is a common view that most migrants come from the poorest strata of society. However, research has shown that this is not the case. Moreover, if we accepted this view, it would be the same as saying that migrants (who are the poorest) send money home to the richer, non-emigrant part of the population. And this would not make sense (Skeldon 2002)[14]. In fact, emigrants usually achieve higher education than those who remain in the country of origin. Most migrants to the OECD countries completed secondary or higher education (see Carrington & Detragiache 1998). This is natural because most migrants need sufficient knowledge and finance to cross borders, whether legally or illegally. The poorest people usually do not meet either of these preconditions.

B3. Development aspects of remittances

Classical migration theories (Massey et al. 1993) see the socio-economic differences between developed and developing regions as the main driving forces that “dictate international migration” (Drbohlav 2001)[15]. The nexus between development opportunities and migration processes creates a complex of relations and impacts that are the subject of the current research. The development aspects of remittances are among the leading research themes.

A whole range of studies consider remittances as a useful tool for the development of economically poor countries, particularly in rural areas (see for example Taylor 1992); some even see them as an alternative development tool. But what exactly are remittances?

Put simply, remittances are transfers of money or goods from migrants living abroad. Statistical data published by the International Monetary Fund (IMF) identifies three categories of remittances. However, both generally and in specialised literature on remittances there is a tendency to use the term remittances in the sense of the first category (Gammeltoft 2002)[16].

• Workers´ remittances are transfers of goods and finances from workers who remain abroad for a period of one year or longer;

• Compensation of employees are transactions from persons who remain abroad for a period shorter than one year;

• Migrants’ transfers are flows of goods and funds linked to cross-border migration (for example, daily commuting to work across borders)

Other classifications of remittances are based on distinguishing among types of remittance senders and receivers. Carling (2005) identifies seven distinct remittance forms:

1. Personal deposits or investment – money transfers for personal use (investment, consumption, entrepreneurial development, home building, purchase of land, savings, etc.). Migrants themselves directly control the use of the expenditure.

2. Intra-family transfers - money sent by a migrant to his/her relatives or friends in the country of origin. In most countries these are the most important remittance flows, often sent on a regular basis (on a monthly basis or on the occasion of an event important for the family, religious festivities, etc.). This remittance type covers the basic subsistence needs of the family: expenditures on food, education and health care services. Remittance receivers most often decide how the money is put to use.

3. Charity donations – used for charitable purposes, sent to churches and mosques.

4. Collective investment aimed at promoting development – the most frequent fund transfers from migrant organisations abroad, which should stimulate community development in countries of origin.

5. Taxes and deductions – obligatory contributions flowing to public institutions such as schools and hospitals in order to secure education or health care services for family members and friends in the country of origin.

6. & 7. Old age pensions and other transfers related to social security services[17] – these comprise regular transfers from former employees, pension funds and the governments of countries where a migrant was employed.

Monetary remittances are sent through a large number of transfer mechanisms. Carling (2005)[18] mentions seven remittance transfer methods:

1. Electronic cash transfers (cash-based systems)

2. Electronic fund transfers from one account to another (account-to-account systems)

3. Transfer of funds using (microchip) cards (card-based systems)

4. Transfer of funds using paper documents (cheques, bills of exchange, cash vouchers)

5. Informal Value Transfer Systems (IVTS)[19]

6. Personal couriers

7. Remittances in kind

As with many other migration-related issues, remittances are very difficult to measure. There are estimates for remittance volumes but it is important to highlight that these estimates are based largely on funds sent through formal channels. According to research (quoted in Puri & Ritzema 2001)[20] carried out predominantly in the 1980s, the estimated volume of remittances sent through informal channels represented between 8 and 85 percent of the total official remittances flow, varying from country to country. Remittance statistics do not include these figures.

The economic distribution of remittance inflows shows that developing countries are the dominant remittance receivers, with middle-income countries being the largest and low-income countries the smallest receivers. This ratio has remained flat over the last decade.

The geographical distribution of remittances in the last nine years indicates that Sub-Saharan Africa has received the lowest volume of remittances, compared to Latin America and the Caribbean, and East Asia and the Pacific (see details in Table B.2). No significant changes in this trend are expected in the foreseeable future.

Table B.2 Distribution of workers’ remittances, employee compensation and migration transfers according to individual regions in 2001 – 2008 (in $ billion).

|

Region |

2000 |

2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

2007 |

2008* |

|

East Asia and Pacific |

16.7 |

20.1 |

29.5 |

35.4 |

39.2 |

46.9 |

52.9 |

65.2 |

69.9 |

|

Europe and Central Asia |

12.8 |

12.4 |

13.7 |

15.5 |

22.2 |

31.2 |

38.3 |

50.4 |

53.1 |

|

Latin America and Caribbean |

20.0 |

24.2 |

27.9 |

36.6 |

43.3 |

50.1 |

59.2 |

63.1 |

63.3 |

|

Middle-East and North Africa |

12.9 |

14.7 |

15.2 |

20.4 |

23.0 |

24.3 |

25.7 |

31.3 |

33.7 |

|

South Asia |

17.2 |

19.2 |

24.1 |

30.4 |

28.7 |

33.1 |

39.6 |

52.1 |

66.0 |

|

Sub-Saharan Africa |

4.6 |

4.6 |

5.0 |

6.0 |

8.0 |

9.4 |

12.9 |

18.6 |

19.8 |

|

Developing Countries |

84.2 |

95.2 |

115.5 |

144.3 |

164.4 |

194.8 |

228.7 |

280.7 |

305.3 |

|

World |

131.5 |

146.8 |

169.5 |

207.3 |

234.9 |

267.8 |

306.6 |

370.8 |

397.0 |

* estimations

Source: World Bank (2009)[21]

The statistics clearly illustrate the increasing importance of remittances in the economies of developing countries. But what is the link between remittances, development and poverty in the areas where migration originated? The complexity and range of this highly interesting topic makes any in-depth analysis of the issue in this chapter impossible. Still, let us look at the conclusions of studies by acknowledged authors.

Remittances naturally improve the standard of life of receivers, with a development impact at the local level through classical multiplier effects, even if they are used for consumption “only”. Therefore, this type of remittance use could be considered a development tool with regard to secondary effects of increased consumption which are important, for instance, in creating local job opportunities. Studies by Adams & Page (2003)[22] uncover statistical proof of the positive impact of remittances on poverty alleviation in developing countries, without concentrating on the use of remittances. Besides, remittances invested in the construction of new infrastructure, schools, community centres, houses, etc. improve and modernise local economic activities, and/or enable the establishing of new small enterprises that could stimulate or sustain development.

Ellis (2003)[23] has come up with five fundamental ways in which remittances may help to reduce people’s vulnerability and poverty. Remittances mainly facilitate:

1. Investment in land or improvement of its quality;

2. Cash purchase of agricultural inputs (e.g. hired labour, control of diseases) with a view to using more effective cultivation methods and gaining higher revenues;

3. Investment in agricultural equipment (e.g. water pumps, ploughs, etc.);

4. Investment in education to secure better opportunities for future generations;

5. Investment in property (assets) with a view to generating profit in the place of residence, but outside the agricultural sector (e.g. a rickshaw, a hammer mill, a shop).

Studies also outline the negative attributes of migration and remittance sending. For example, according to Gammeltoft (2002), remittances may delay the necessary structural reforms and cause and/or increase the dependency of the population and local economy on remittances. Also, the absence of a parent in a family may have negative social impacts.

In this context, Skeldon (2005)[24] highlights the fact that remittances cannot be perceived as a universal panacea for poverty alleviation. Only a relatively small number of migrants cross international borders and even when they decide to become international migrants, they often come from a limited number of areas in a given country of origin. Therefore, according to Skeldon, international migration cannot be the crucial factor in the process of poverty alleviation at the national level.

B4. Conclusion

Throughout the history of mankind, national and international migration has been an integral part of survival strategies and has provided a means of improving the quality of life. Restrictive migration policies in economically advanced countries cannot change anything about this and these restrictive policies are the reason why the development potential of international migration cannot be fully exploited, both in advanced and developing economies. Further, restrictive policies, which close down opportunities for legal migration, often shift problems into the area of illegal migration. Illegal migration drains budgets in destination countries and negatively influences the perception of migrants by majority societies (Stojanov & Novosák 2008)[25].

Remittances constitute a significant component of international finance flows and have a profound impact on economic potential, both in macroeconomic and microeconomic terms (Ellis 2003). Remittances offer some interesting tools for stimulating development in economically poor countries. However, the relation between these two topics is very complex and it includes many other issues, such as the migration of skilled persons, and return or circulation migration. This chapter focused on a brief overview of remittances and selected development issues relating to remittances, reaching a general conclusion that international migration flows in the form of remittances have predominantly positive effects on the development of economically poor regions.

C) What do we know about remittances sent from the Czech Republic: previous and planned research

Pavlína Šolcová

Faculty of Regional Development and International Studies, Mendel University in Brno

C1. Introduction

The importance of remittances as a tool of economic development in poor countries – which are dominant remittance receivers according to the distribution of remittance inflows – has been increasingly recognised by development and migration studies in the Czech Republic in recent years.

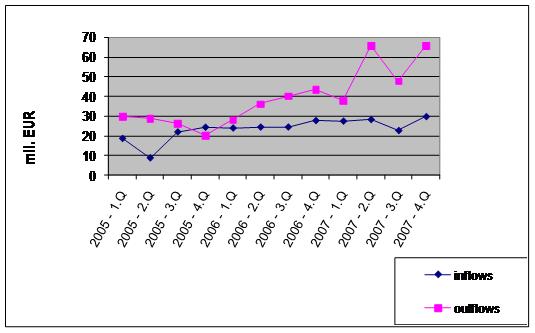

Statistics show that the Czech Republic became a net-sender of remittances in 2006 (see graph C.1). In 2005-2007, the majority of remittances were transferred to the Slovak Republic, Ukraine and Vietnam. The Czech Republic has become an attractive destination for foreign migrants, with about 440,000 foreigners registered as legal residents in 2009, accounting for around 4 percent of the total population of the country. Besides migrants from the Slovak Republic, most foreigners come from Ukraine, Vietnam, Moldova and Russia. According to the World Bank, remittances from the Czech Republic reached about 55 billion Czech crowns in 2007, that is 2 to 2.4 percent of the country’s GDP (see details below). The funds were chiefly transferred to Slovakia (37%), followed by Ukraine (28%), Vietnam (11%) and Poland, Moldova, China, Mongolia and other countries (the remaining 24 percent). There is no data available on the average costs of remittance-sending. Estimated costs range from 6 to 18 percent.

It remains to be seen how remittance flows will change in the face of the economic crisis. For the time being, there are only estimates. In its latest reports, the World Bank estimates that in 2008 the total value of remittances worldwide was $305 billion. Flows from the EU countries have increased by 60 percent since 2004 (to EUR25 billion), but in 2009, the volume of remittances is expected to fall sharply largely due to job losses among migrants. The situation is especially problematic in countries where income from remittances constitutes a large part of GDP[26].

Table C.1 Remittances (average

2005-2007)

|

Money inflow (%) |

Money outflow (%) |

|||

|

Country |

Germany |

36 |

Slovakia |

37 |

|

Austria |

25 |

Ukraine |

28 |

|

|

UK |

24 |

Vietnam |

11 |

|

|

USA |

6 |

Poland |

9 |

|

|

Switzerland |

3 |

China |

4 |

|

|

Other |

6 |

Other |

11 |

|

|

Total |

100 |

Total |

100 |

|

Graph C.1 Developments in remittance inflows and outflows (2005-2007)

Source: the Czech National Bank (CNB), compiled by the author

C2. Selected earlier research on remittances in the Czech Republic

The issue of remittances is often mentioned in research reports or other publications. However, few of these were specifically concerned with the situation in the Czech Republic. Works by R. Stojanov and Novosák[27] as well as Ondřej Horký[28] analyse the topic at a theoretical level. Horky has criticized the inaccessibility of data: “The relationship between migration and development is not quite clear mainly because of the lack of data … In the Czech Republic we do not have reliable data on any of the phenomena. Hence, potential coherence or incoherence between immigration and development policies may only be estimated.” In his text, Horký outlined the following recommendations for public institutions dealing with migration issues (and remittances):

• The Czech Ministry of Labour and Social Affairs (MPSV) to carry out a critical analysis of the development potential of temporary migration in the Czech Republic;

• The Finance Ministry to continuously monitor out-remittances and produce high quality statistics on their volume and territorial distribution; in cooperation with banks and other financial institutions to facilitate fund transfers to migrants’ countries of origin;

• The Minister for Human Rights to aim to acquire status for significant ethnic minorities in developing and transforming countries that have no such status so far; in cooperation with other players to engage diaspora on the development cooperation programme.

Marie Říhová of the International Organization for Migration considers searching for earlier research projects on remittances (back to 2007) a wild-goose chase, as no such large-scale projects exist. Yana Leontyieva of the Institute of Sociology of the Czech Academy of Sciences agrees with this opinion. She also mentioned a research project commissioned by the Czech Labour and Social Affairs Ministry, which focused mainly on the level of education and qualifications of migrants and their intentions concerning their stay in the Czech Republic[29].

The survey contained two questions related to remittances. Results provided information about:

• The percentage of foreigners who send money to their countries of origin.

Table C.2: Q33. Do you send money back to your family or relatives in your home country?

|

Yes |

62 |

|

No |

38 |

N = 1011, no answer 1

• Dependence of families on the money sent.

Table C.3: Q34. How important is the money you send home for your family?

|

They cannot make ends meet without the money, they are dependent on it. |

46 |

|

They aren’t totally dependent on the money, but it significantly improves their livelihood. |

44 |

|

They could live without the money; it augments their income. |

10 |

N = 630, no answer 1 (Source: documentation provided by Y. Leontiyeva)

Remittance sending according to selected characteristics of respondents (age, sex, nationality, etc.) – based on the research results, Y. Leontiyeva outlined the following remittance-related hypotheses:

• Remittance sending depends on the character of migration, migrants’ plans and their intention to settle down in country of destination;

• Migrants’ economic situation and their position on the labour market of a host country play an important role in remittance sending; research has shown that highly qualified migrants send lower amounts of money;

• Apart from economic reasons, remittances are also influenced by the situation in migrants’ families, especially by divorces resulting in the departure of husbands or separation of parents from their children;

• Older migrants often support families in their countries of origin to a greater extent than the younger ones. However, it is important to differentiate between this factor and the situation in families;

• A strong correlation between sex and remittance sending was registered; research results have indicated that men are more often the breadwinners than women;

• Remittance-related behaviour of migrants varies with nationality.

The researcher has made the following recommendation: “If we take into consideration the latest findings and the fact that migrants from various countries are often differently concentrated in regions of the country of destination, research into remittances should cover specific locations with a high concentration of groups of selected migrants (since, for instance, the Vietnamese are concentrated in different regions than the Ukrainians and Russians).”

According to Dušan Drbohlav from the Charles University, one of the projects dealing with the issue of remittances indirectly is the study named “The risk of possible outflow of qualified experts from the Czech Republic abroad”[30]. Although focusing on remittances sent by Czech citizens living abroad, the study analyses the costs and benefits of remittances for countries of origin (questions such as expenditure on education, the effects of fund re-transfers, knowledge sharing, etc.), and the impact of the outflow of qualified experts on the economy and competitiveness of destination countries. In a similar way, we could comment on other research projects, concentrating mainly on Ukrainian and Russian immigration to the Czech Republic, but none of them dealt specifically with the issue of remittances.

The key project on remittances in the Czech Republic, which has particularly interested the public authorities, was “A review of the market for remittances in the Czech Republic on the basis of the CPSS - World Bank „General Principles for International Remittance Services”.[31] In May 2008, at the request of the Finance Ministry of the Czech Republic, a team of World Bank experts conducted research on the market for remittances in the Czech Republic on the basis of the general principles set out by CPSS – World Bank[32] through a series of interviews. These interviews were mainly with representatives of the Czech Statistical Office (CSU), the Czech National Bank (CNB), the Czech Interior Ministry (MV), the Czech Finance Ministry (MF), the International Organization for Migration (IOM), the Czech Banking Association and the Charles University (UK). The team recommended a set of measures to reduce the costs of remittance transfers and make remittance-sending generally safer and more efficient. (A note from the author: the economic crisis has certainly changed the situation; hence some of the information mentioned below may not be current).

• A CSU representative informed about the long-term tradition of wage monitoring by the Czech Statistical Office and the crucial differentiation in the CSU records between resident and non-resident migrants[33]. He mentioned that in 2008 the CSU planned to prepare a review of data and calculation of remittances (usually a competence of the CNB, this year delegated to the CSU). The information needed for calculation is obtained mainly from the MPSV, the MV and local employment offices, the Czech Police, the Czech Industry and Trade Ministry, the Ministry of Foreign Affairs and the Education Ministry. As of 2005, the records of employed foreigners in each firm have to be kept separately on the basis of their (non-) residence in the Czech Republic.

• The Czech National Bank has no reliable data on the means of sending remittances. It is estimated that about one half of the volume is transmitted through the banking system and the other half is channelled through other money transfer providers. The CNB has been discussing this issue with its partners, concentrating mainly on the new methodology of remittance calculation. The CNB has tried to consult with central banks of other countries on the issue of remittances but, unfortunately, these institutions have been facing the same problem. In the words of a CNB representative: “…it is thus very difficult to tackle the issue of remittances in a comprehensive and appropriate way.”

• Representatives of the MV mentioned projects concerning migration as part of the EU’s Eastern Neighbourhood Policy in Moldova, Ukraine, Serbia, Western Balkans, Georgia and Bosnia-Herzegovina, which started as early as 2001 – 2002.

• The Financial Analytical unit of the Czech Finance Ministry outlined a new law on anti-money laundering and the fight against the financing of terrorism[34].

• The International Organization for Migration (IOM) has been dealing with the issue of remittances at an international level. In this regard, the organisation has carried out small missions in selected countries (Georgia, Mongolia, Iraq and Serbia) as a part of a project that started about four years ago, which has provided valuable experience from work among migrants coming from Mongolia, Moldova and Ukraine, among others.

• Representatives of the Czech Banking Association mentioned that remittance use varies from country to country. For example, Vietnamese migrants tend to also send remittances home for entrepreneurial reasons, aside from the purpose of subsistence.

Results of the World Bank report were presented during a public

seminar organised by the Czech Ministry of Finance on

The report provides an evaluation of the application of five main principles set out by the CPSS-World Bank in the Czech Republic. A set of recommendations is outlined in the following table.

Table C.4 Selected recommendations of the World Bank for the Czech Republic on the basis of General Principles for International Remittance Services

|

General Principles (P 1-5) for International Remittance Services |

Recommendations for the Czech Republic |

|

P1 (transparency and consumer protection): The market for remittance services should be transparent and have adequate consumer protection. |

Studies about migrants should be carried out in the Czech Republic (cooperation among public authorities, universities, NGOs, etc.) that would map basic features of the market for remittances. Public authorities should collect and publish data on fees, foreign exchange rates, and further information related to remittance sending. Consider setting up an information telephone number for migrants or a database accessible to the public, providing comparative price information about remittance sending. Undertake campaigns and programmes promoting financial literacy. |

|

P2 (payment system infrastructure): Improvements to payment system infrastructure that have the potential to increase the efficiency of remittance services should be encouraged. |

It is important to aim at stricter requirements concerning transparency of transfers to countries outside the EU (legal framework, cost of remittance sending). Explore the possibilities of the use of payment cards and advocate ever greater use of ATM and terminal networks by remittance service providers (RSPs); analyse the possibility of payments via Internet or a mobile phone. Reach agreement at a national level and introduce a common methodology for the calculation of prices of remittance services to make it clear for migrants what is included in the price. Reform of nation-wide postal services, including the modernisation of the telecom infrastructure and operations procedures. |

|

P3 (the legal and regulatory environment): Remittance services should be supported by a sound, predictable, non-discriminatory and proportionate legal and regulatory framework in relevant jurisdictions. |

Establishment of a legal framework on the basis of the principles set out by the World Bank – in the process of adaptation of the Czech legal system to the European environment. Finalise prepared reforms and establish adequate regulation governing national payment systems. Explore the possibility of setting out specific rules and procedures concerning remittances with international applicability, including countries of the EU. |

|

P4 (market structure and competition): Competitive market conditions, including appropriate access to domestic payment infrastructures, should be fostered in the remittance industry. |

Pay attention to the dynamics of the market for remittances, based on market research carried out in the future. Continuously monitor whether conditions for entering the market are fair. Undertake campaigns with a view of increasing the number of persons remitting funds through regulated channels. |

|

P5 (governance and risk management): Remittance services should be supported by appropriate governance and risk management practices. |

Remittance service providers in the Czech Republic use their own manuals and employ trained staff, but there is no oversight (except for RSPs under the direct oversight of the CNB), or a continuous control of their procedures. A specialised institution should be established in this regard. Rules of regulation should be set out that would protect rights of users of remittances or other cross-border payments. A financial arbitrator should have the adequate competence and authority to settle disputes arising from abusive conduct or the RSPs´ insolvency. |

Source: World Bank report, compiled by the author

The following is a list of remittance-related events in the Czech Republic:

• Seminar

by the World Bank (

• Seminar

organized jointly by the Multicultural Center Prague (a member of FoRS)[36]

and the Ministry of Finance (

• Seminar

by the CSU (

National accounts use the definition of remittances provided by the balance of payments that sees remittances as the total volume of transfers from household to household: the net income of non-resident households from persons working abroad for less than one year, transfers from foreigners to residents, and transfers from other citizens. Unfortunately, the banks’ statistics cannot capture remittance flows. There are no records of sale/purchase of foreign exchange, and the CNB only keeps records of money flows through payment cards.

C3. Further developments (new projects, research studies, etc.)

Projects of the Ministry of Finance, supervised by the World Bank

The above-mentioned report highlighted the increasing importance of remittances. It is in the general interest of the Ministry of Finance, the institution which commissioned this study, to comply with the outlined recommendations. In this connection, crucial actions should be taken with a view of strengthening the efficiency, trustworthiness and transparency of the national market for remittances. The World Bank put forward five possible remittance-related projects: a survey of the market for remittances, a national remittance database, participation in the reform of the legal and regulatory framework, educational campaigns for migrants, and the training of specialists. Based on consultations with the World Bank, the Finance Ministry decided to carry out a survey of the market for remittances and set up a national database on remittances.

• Survey of the market for remittances – a survey will be conducted under the supervision of the World Bank, in cooperation with the Finance Ministry, consulates and embassies. Results will be presented at a seminar whose primary focus will be to share collected data with specialists, other stakeholders and migrants.

• Setting up a national database that will provide data on the costs of remittance sending – this will include detailed monitoring of remittance flows and the cost of remittance sending (including exchange rates). The database should be updated about twice a year[37] and should bring more transparency into remittance services, raise the awareness of clients and possibly increase competitiveness and reduce fees. The World Bank, the Finance Ministry and other stakeholders will participate in the project.

According to Donald F. Terry of the World Bank, a final report summarizing the results of the survey of the market for remittances should be released in autumn 2009 and the database on remittances should be launched in spring 2010. Although the Czech Republic has become an attractive country for international migrants, there is currently no information source on remittance prices that migrants could use. According to the Ministry of Finance and the World Bank, the Czech Republic could become a source of knowledge and experience for neighbouring countries in the future.

A Czech Statistical Office project

V. Ondruš, director of the Department of Annual National Accounts of the Czech Statistical Office, outlined the establishment of a Working Group on the Impacts of Globalisation on National Accounts[38], operating under the umbrella of the UN Economic Council for Europe, whose task is to prepare methodological guidelines concerning remittances, the migration of workers and electronic and transit trade by 2010. The Eurostat was another body to identify the growing significance of remittances. The CSU has applied, together with Eurostat, for a grant to conduct a research project on remittances in 2010 that would analyse the expenditure behaviour of individual migrant groups. The Czech statistical authority has formed a working group consisting of Czech experts who will analyse the research.

A Charles University project

If the Grant Agency of the Czech Republic approves the research proposal of D. Drbohlav, a research project that aims to explore the impact of Ukrainian migration on the Czech Republic will be carried out. The research should also cover the issue of remittances (the volume, mechanisms and conditions under which they are acquired, transmission and the final use of these funds). Quantitative and qualitative research tools will be applied (mainly interviews and questionnaires), with a focus on Ukrainians working in the Czech Republic and the families they have left behind.

C4. Recommendations and critical remarks

In the final part, some select recommendations and critical opinions on earlier and future research and policy measures are presented.

• Reactions of experts to the World Bank’s review of the market for remittances in the Czech Republic

- According to L. Vacková (from the CSU), the World Bank data on the value of remittances in the Czech Republic are only gross estimates as they were derived from inaccurate data provided by the CNB. This is a consequence of a general absence of a consistent methodology for calculation of remittances and a lack of necessary data.

- The Czech Banking Association points to the fact that findings in some parts of the report are generalised to such an extent that significant differences in the functioning of remittance services, the level of regulation and supervision, as well as differences across areas become blurred. Problems often have their roots in the remittance-receiving countries and therefore, in some cases, it is unlikely that they will be influenced by the proposed measures. The recommendations proposed by the World Bank have their flaws – a one-size-fits-all perspective prevails and little consideration is given to the differences between subjects under strict supervision and other RSPs. Little attention is devoted to the fact that the Czech Republic will implement legislation (Act No. 253/2008 Coll. on certain measures against the legalisation of revenues from criminal acts and financing of terrorism, or the Payment System Act[39]), which will influence the functioning of RSPs in a fundamental way.

- Marie Říhová (IOM) states that the amount of remittances that legal migrants have sent through informal channels is far greater than portrayed in the report. In the Czech Republic there is a lack of finance-related literature for migrants. It is also important to pay more attention to the training of employees in the public and banking sectors. The report does not tackle the development impact of remittances on developing countries and the interconnectedness of remittances and development projects.

• General remarks

- According to Marie Říhová, it is necessary to engage migrants in future projects and focus also on development potential. Leila Rispens-Noel (from Oxfam Novib) expressed a critical view of the database on remittance prices in the sense that even if migrants had the information about the prices of sending funds through various institutions, their choice would be limited by the presence of a given bank or provider in the remittance destination. A tricky question remains how to involve illegal migrants in legal sending of remittances. L. Rispens-Noel also took a negative stance towards the use of new technologies, such as mobile banking, as they cannot be used in countries that lack basic infrastructure.

Acknowledgements:

I would like to express my gratitude to M. Rihova (the IOM), Y. Leontyieva (the Institute of Sociology of the Czech Academy of Sciences), Doc. Drbohlav (the Faculty of Natural Sciences of the Charles University) and Leile Rispens-Noel (Oxfam Novib) for providing me with valuable information.

D) Sending Remittances from the Czech Republic to the Country of Origin

Report from a Research Investigation

Blanka Tollarová and Tereza Rejšková

Multicultural Center Prague

D1. Introduction

This chapter comprises a report from a research investigation into remittances sent from the Czech Republic to migrants’ countries of origin. Our investigation provides a fundamental insight into the financial market for remittances: we show how migrants sent money to their country of origin, the costs that they incurred and the alternative forms of transferring remittances that are available. The estimates of world-wide remittance flows are astonishing. Hence, remittances have become an interesting economic and financial topic. The investigation highlights the importance and social value of remittances: remittances not only support migrants’ families and relatives or increase their standard of living; they also help to strengthen family ties and add new dimensions to relationships between relatives. The final part of this chapter and the introductory part of the study are devoted to the last important thematic focus of our investigation – the role of the non-governmental sector in addressing the issues associated with remittances.

With regard to the context of this project – tackling the development impact of remittances – our investigation focused exclusively on sending remittances to developing or transforming countries outside the EU. It has to be pointed out that this report does not represent any kind of extensive and representative research. Our main objective was to map the field and identify some current themes related to remittance-sending in the Czech Republic. We thus see our work as forming the pilot phase of a potential more extensive research project on remittances, which is yet to be carried out in the Czech Republic.

D2. The research process and methodology

Data on remittance-sending was collected over a period of eight weeks between December 2008 and February 2009.

D2.1 The research technique

When planning the research investigation, we considered the use of structured and semi-structured interviews, or alternatively, focus groups from the very beginning.

For the purposes of this study, we defined remittances as funds sent by migrants to their country of origin. We did not take into account international trade transactions or payments for goods and services related to entrepreneurial activities. Remittances were understood primarily as intra-family transfers, either in the form of regular sums of money (parts of migrants’ wage), or in the form of less regular or irregular money transfers sent home on various occasions.

The available literature on remittances and current trends in development projects, particularly with regard to measures that should make sending remittances easier, influenced our choice of thematic areas:

1. How do migrants send money from the Czech Republic to their country of origin?

2. What are the costs of remittance-sending and who bears them?

3. What are the social aspects of sending and receiving remittances?

4. What means can be used to inform migrants about different ways of sending money, further, what means can be used to influence them or change the ways of sending?

On the basis of these thematic areas and a questionnaire prepared by the World Bank for the general purpose of remittance research, we designed an interview schedule. However, we tried to be flexible; interviews also allowed room to pursue other thematic areas and cover other dimensions of the examined problem than those outlined in the schedule. As the size of our sample was relatively small, we did not concentrate on determining the exact volume of remittances. Instead, we were interested in the amounts of money sent and the frequency of money transfers. Given the sample size, it was clear to us from the beginning that the collected data would not allow for any general conclusions to be drawn. Hence, we did not focus on this purely financial information, and many respondents apparently appreciated this approach. Numerical data provided in this report should be understood as examples rather than statistically relevant findings that are generally applicable to the population of migrants in the Czech Republic.

We noted migrants’ responses down directly in the course of the interviews and, in some cases, audio recordings were made to capture the details of responses we received from interviewees.

Besides interviews, observations from the field were another important source of information. In many cases, interviews were not conducted according to the outlined schedule; instead data was obtained on the basis of personal contacts, via telephone or e-mail. Some informers played the role of intermediaries or gatekeepers (those opening the door to persons who take part in a research interview and share information), but at the same time, they provided us with valuable data. Some migrants did not want to be formally interviewed, but they were willing to discuss some remittance-related topics informally, outside the interview. There are a number of reasons why migrants refused formal interviews, the main being: the sensitivity of all questions concerning migrants’ finances; intra-family financial flows; and social contacts established on the basis of financial matters. This is why we often obtained information by talking about the experiences of other migrants rather than the personal experiences of respondents (although, in fact, respondents may have been talking about their own experiences). In our opinion, this highlights the sensitivity of the topic: giving information about other people was easier than talking about one’s own affairs.

D2.2 Identifying participants

We identified and contacted three categories of respondents: 1) representatives of Czech non-governmental organisations (NGOs) whose field of action is the provision of assistance and counselling services to migrants; 2) representatives of migrant organisations and associations; 3) migrants who send money to their country of origin. The sample comprised representatives of the main nationalities of migrants living in the Czech Republic (and coming from outside the EU) – Ukraine, Russia, Moldova, Mongolia and Vietnam. Ultimately, we also included a small number of respondents from Belarus and informers from China.

A formal interview was conducted with 17 migrants. A further 15 migrants gave us brief information about their strategies of remittance-sending or provided us with important information (for example, interpreters, migrant employers, immigrants who opened the door to further contacts). The respondents come from the city of Prague, Ústí nad Labem and Pilsen.

Tracing suitable respondents was a more difficult task than we expected. As a rule, NGOs specialising in the provision of counselling services lack meaningful knowledge of the remittance issue. They do not deal with it very often, because clients do not turn to them with remittance-related concerns. None of the addressed NGOs is specifically involved in this field. We fared better with migrant organisations and associations for two reasons. First, representatives of these organisations were migrants themselves and thus had personal, firsthand experience with sending remittances, and second, a number of migrant organisations have professional experiences with companies specialising in international money transfers.

We searched out individual migrants using snowball sampling techniques, using the social contacts of various initial intermediaries: friends, doctors, interpreters, shop assistants, journalists and others. We tried to trace migrants with diverse backgrounds in terms of length of stay in the country, job position or their level of integration into the majority society.

In general, we found it relatively easy to gain information about remittances from representatives of organisations and individual migrants from Ukraine and Russia. We did not experience any communication problems or reluctance to disclose information on sending remittances or their use. By contrast, we encountered difficulties when communicating with migrant organisations and individual migrants coming from Asia, namely Vietnam, China and Mongolia. Information was also difficult to obtain from the respective representatives of these migrant communities, perhaps due to cultural differences in how this kind of information is discussed; most informers stated that their countrymen do not discuss this topic among themselves. They do not talk about it even with friends, less so with researchers – representatives of the majority society. Except for two individual interviews, we had to rely on information provided by the intermediaries who collected data for us, making use of their contacts with migrants from Vietnam, China and Mongolia: interpreter-migrants, migrants that are well-integrated in the majority society or Czechs engaged in activities supporting these communities.

D3. Sending Remittances from the Czech Republic to country of origin

D3.1 What are remittances?

Our investigation revealed two relevant forms of remittances – money and goods. However, this does not mean that other forms of remittances are not relevant to migrants staying in the Czech Republic. The limited sample size does not allow us to quantify the volume of remittances sent home in monetary and material form, but responses indicate that migrants view the sending of both money and goods as important and interconnected.

The goods sent across borders comprise items that are unavailable or expensive in the country of origin (digital devices, quality groceries, delicacies), as well as cosmetics, clothing, shoes and other goods of day-to-day consumption, or gifts and trifles (items typical of home country, crosswords etc.) The culture of gifts proved to be a strong motivation factor for sending remittances: a large number of migrants regularly send gifts to their relatives. Presents are symbols of social ties and the intensity of social contacts, rather than economic support (although this aspect is often also taken into consideration, because presents may be very expensive). Also, the early experiences of migrants (usually gained in the country of origin) and their being practical lead to maximum use of items in migrants’ households or households of their relatives.

Some migrants compare the prices of goods in the Czech Republic with the prices in their country of origin and send home items that are significantly cheaper in the Czech Republic (oil, cosmetics, clothing bought at discounted prices). Some of the items sent to the country of origin are further distributed or otherwise marketed. For example, migrants buy many pairs of shoes, family members keep those pairs that fit them or that can be used within the household and the remaining pairs of shoes are sold to neighbours. The high importance of sending items back may be explained by the fact that these items help to extend social contacts and, in a way, emphasize the quality of the migrants’ social ties.

D3.1.1 Sending in both directions

Our investigation shows that many migrants see the flow of remittances from the opposite direction as equally important. Although the primary focus of the project was on remittances sent by migrants to their country of origin, it is important to bear in mind that some migrants receive, at least at some point during their stay in the Czech Republic, financial support from their family in the country of origin. Flows of money and goods in both directions often provide the framework for respondents’ perceptions concerning remittances: some migrants only send home regular sums (part of their wage), while many others view sending and receiving in both directions as essential.

We discovered a number of reasons for sending money to migrants living in the Czech Republic. One of them can be the sale of property in the country of origin and subsequent transfer of funds to the migrant’s country of current residence. Another reason may be the direct financial support of migrants by their families. This is also the case among migrants coming from poor countries, such as Vietnam or Mongolia, when they are exposed to sudden job loss, illness or other unfavourable circumstances. Migrants finding themselves in these situations often use the services of fast international transfer providers and obtain money from home that will help them to get through the difficult times and cover living expenses (such as rent or medical treatment fees) until they find a new job. Some immigrants who reside in the Czech Republic permanently earn relatively low income (for example successful applicants for asylum or workers employed in low-skilled occupations), and are therefore supported on a regular basis by relatives in their country of origin, both in monetary and material terms.

Many goods that are sent to migrants in the Czech Republic by their families represent material relief: for example, some clothing items (underwear, hosiery) or toys for children are cheaper outside of the Czech Republic. At the same time, migrants receive gifts that have identity-related or emotional significance – migrants like to have a cup of “their tea” or want to wear something sent from home (“I’m wearing part of Belarus.”). These material remittances may not have great economic value - they are mentioned due to their context. Most respondents described remitting money and items home as an intensive two-way flow. What they find meaningful is the cyclical and dynamic nature of this cross-border movement.

D3.2 The means of sending remittances

This section focuses on financial remittances and financial institutions that help to transfer funds to remittance destinations. Each migrant who sends remittances has his/her own way of optimising money transfers: how to transmit funds, which currency to exchange money in and which currency to get hold of the money in at home. Whether the transfers are made on a regular or one-off basis, over time each migrant develops a routine that he/she considers to be reliable. The way in which migrants send remittances home depends on many circumstances. The sums transferred vary and the reasons for choosing a particular way of sending remittances are complex. The status and experience of a migrant in the new society as well as the place of residence of the migrant’s family or remittance end users are also influential factors.

Many migrants seek comparative information on remittance-sending, compare offers by the providers of financial services and consider the amount of money to be sent as well as the accessibility of branches or agents. Other aspects taken into consideration include the costs of remittance-sending and the ways of getting hold of the money in a migrants’ country of origin. Other migrants follow the example of their friends, relatives, and countrymen. Naturally, migrants share and discuss their experiences, comparing best practice within migrant social networks. Some migrants send remittances in a way recommended to them by their employers or clients (job intermediaries, often illegal or semi-legal). Some recruitment agencies have begun to treat their employees in a “sustainable” way: apart from a job and accommodation, they also arrange remittance-sending, with the conditions of transfer being continuously optimised. In doing so, the agencies gain, among other things, the trust of migrant workers and relatively positive feedback. It is thus more likely that the workers continue to use the services of these agencies. Respondents mentioned that many migrants – especially those who intend to work temporarily in the Czech Republic, earn money and return home – prefer to employ a client or an agency to make all the necessary arrangements on their behalf. These migrants are ready to follow the agency’s instructions and advice, often without attempting to understand the process. This also applies to the market for remittances.

The ways of sending remittances are divided into three categories according to the extent to which the services of official and established institutions are used: 1) formal way – using the services of well-established financial institutions; 2) informal way – physical transfer of cash by migrants themselves or other persons; 3) various combinations of formal and informal ways.

D3.2.1 Official financial institutions: companies specialising in international money transfers, banks, post offices

Despite the limited sample size, we managed to encompass the most important financial institutions offering international transfers of funds into our investigation. In principle, remittances are sent through companies specialising in international money transfers, banks and post offices. Our aim here is to give only a brief overview of the notable features of individual money transfer providers and the reasons that migrants choose their services, rather than to provide a comprehensive list of providers operating in the Czech market. There are multiple companies providing remittance services that are easily accessible, especially to those living in urban areas. Accessibility and price are among the main criteria applied by migrants when choosing financial institutions for sending remittances.

Companies specialising in international money transfers

These companies offer one-off international transfers of funds: the client deposits money with a branch or an agent, gives the name of the receiver and obtains a transaction number, which he subsequently discloses to the receiver. At an agreed time, the receiver goes to an agreed branch or agent in the remittance destination, shows the transaction number or identifies himself/herself, and picks the money up.

Companies that specialise in international money transfers are a symbol of security for migrants. Some migrants exclusively use the services provided by these institutions, others use them from time to time or prefer informal ways of sending money. Still, migrants using informal channels are aware that there is always the option to use the services of an official provider if they need to send or receive money fast and/or the informal channel that they usually use is not available. Compared with banks, the fundamental advantage of these companies is that clients are not obliged to show identity cards, which enables migrants in an irregular position to use their services. In addition to the advantage of specialisation in transferring money and no requirement of registration, the fact that there are no conditions regarding the use of other contract-based services (such as bank account) is appealing to many migrants.

The fees charged for international money transfers are set in such a way that it is inconvenient to send small amounts of money. According to the companies’ websites, fees, particularly for sending higher sums (over $1,000, also for lower amounts sent to Asia), range from 2.5 to 4 percent of the transferred amount; fees for lower sums reach between 8 and 16 percent. All fees are set for intervals (for example the transfer of EUR50 – EUR100 costs x percent, EUR101 – EUR200 y percent) and decline with the amount of money sent. A fee for sending a small sum falling into the lower part of the interval could reach almost 30 percent. These high costs put many migrants off and support their view that these services are unfavourable. In particular, those who had no personal experience with these companies or had only sent smaller sums stated that companies specialising in international money transfers charge fees reaching about 20 to 30 percent. Naturally, they see the services of these companies as absolutely unfavourable and so do not use them. Past experience probably plays a significant role here, as fees used to be higher.

Respondents who had used the services of these companies considered that the fees were justified by the level of reliability and speed of the transfer. Many of them followed the developments in transfer rates on the market and always aimed to send money in the most convenient way. In the overwhelming majority of cases we investigated, fees are paid by the sender, except in Mongolia, where, according to some informers, receivers are charged fees too. These fees are related to transfers between the capital city and respective regions.

Migrants who came to the Czech Republic with a view of earning money in order to support their families are particularly sensitive about their expenses. Thus, people who tend to send regular small sums ($50 - $100), for which the fees are relatively high, seek cheaper alternatives and use the services provided by companies specialising in international transfers on a one-off basis. Even if they sent larger amounts, which would entail lower fees, the total fees, accumulated over the time of their stay in the Czech Republic, would be so big that they prefer informal ways of sending money. An advantage of these companies is that the transactions are fast and reliable. Many migrants, especially migrant workers who stay in a dormitory or who share an apartment with other people, cannot physically keep money with them since the risk of theft in a dormitory is high and there are also gangs that rob migrants of money on pay-day. Thus they tend to send money home straight after they are paid their wage. The fee is then considered the lesser of two evils.

Apart from fees, there are other costs related to the use of services provided by these companies, namely the rate of exchange between currencies. Different companies have different methodologies for receiving and dispensing money. This is another aspect that influences migrants’ decisions as to whether they will exchange currency with these companies, or individually in exchange offices, or send money through informal channels.

Western Union

Western Union is a large and obvious player on the market for remittances. Many respondents who remit funds via informal channels use Western Union’s rates as a reference basis. Western Union is a symbol of certainty; a backup option that makes it possible to send money abroad if other ways are unavailable. At the same time, there is a widespread view that the company’s rates are high. Western Union branches are easily accessible, as the company co-operates with the Czech Post and therefore also has branches in smaller towns. For instance, one of them is located within SAPA, a big Vietnamese market place in Prague. According to respondents, the dense network of branches also allows easy access in remittance receiving countries. As for the disadvantages, respondents mentioned the fact that money can often be withdrawn only in local currencies.

Chequepoint

The company has an interesting strategy. It establishes branches in the offices of migrant organisations or firms that are willing to include this aspect in their line of business. Individuals may also act as Chequepoint agents, for instance interpreters, who have contacts with other migrants and access to their communities. Respondents maintained that the financial reward is not the main motivation for arranging transfers. Some of the main motives that agents mentioned were the extension of contacts and the possibility to influence migrants. For instance, a large number of migrants, especially migrant workers, come to the civic association Oberig in Ústí nad Labem and the Czech-Mongolian association in Pilsen to use a Chequepoint counter. These migrants would not otherwise have known about these non-governmental organisations. Apart from having their financial transfers arranged, the migrants get updates about the lives of migrants in the Czech Republic, legal job opportunities, accommodation, health insurance, etc. An advantage of this system is that Chequepoint agents (for example in the civic associations of migrants) are willing to accept money at times convenient for migrants, especially after working hours or during weekends.

In countries of origin, Chequepoint co-operates with exchange offices and banks (either their own or on the basis of a contract) which provide money withdrawal services. However banks and exchange offices, and hence, Chequepoint services, are not as easily accessible as Western Union branches. Still, respondents considered it an advantage that remittance users can choose the currency in which they want to receive the money and therefore were able to choose the most favourable exchange rate.

PDW, Anelik

Respondents characterized these two companies as oriented to Russian-speaking clients. They are supposedly reliable and easily accessible in the country of origin.

MoneyGram and UNIStream

These companies were mentioned only by a few informers. MoneyGram services are used for example by migrants from Mongolia. UNIStream focuses predominantly on Russian-speaking clients.

Banking services and the use of a bank account